How I Got A Great Deal By Buying A 'Totaled' Car With A Salvage Title

Just because a car has a salvage title, doesn't mean it's compromised in any meaningful way.

If a car has a salvage title or rebuilt title, it means it has been damaged to the point where an insurance company deemed it a total loss. And while that sounds scary, it could be a great way to get a sweet, sweet deal on the car you want. Here are the steps needed to make that happen.

In September of 2019, I purchased my dream Jeep, a 1991 Jeep Cherokee Laredo with a manual transmission, despite it having a salvage title. That got some readers talking about whether buying a salvage or rebuilt car is a good idea. Between that and a discussion with our resident car buying expert Tom McParland about one of his clients contemplating buying a rebuilt-title Mazda CX-5, I decided it was time to write my take on all this.

Sometimes The Damage Is Nothing To Worry About

Having bought that 1991 Jeep, it's probably clear that I'm not entirely against buying a salvage title car. That's because salvage title cars aren't necessarily in any worse shape than vehicles with clear titles.

A salvage title car is one that's been deemed a total loss by an insurance company, but it's important to make the distinction between "total loss" and "structurally compromised" or "unsafe."

Take my dad's old 2005 Saturn Vue shown above. When I sold that thing back in 2014, it was in borderline mint condition other than the blown internal clutch slave cylinder that caused me to sell it. Even a close inspection by a mechanic would probably not uncover why this car had a rebuilt title.

A few years prior, my dad drove through an intersection without noticing a Mazda3 coming from the right. The little Japanese car rammed into the Vue's passenger-side door. Apparently the Mazda's front-end damage was pretty bad from what my Dad told me, but the Saturn Vue seemed mostly fine.

According to my dad, the insurance company had a nearby dealership look at the Vue, the technician allegedly said the chassis was damaged, and thus, the trusty five-speed, four-cylinder, Theta-platform Saturn was deemed a total loss.

But my dad disagreed with the assessment. He thought his car's door had absorbed nearly all of the impact energy, and — looking at it carefully — he saw no significant frame damage (my own inspection concluded the same thing). So he kept his Saturn, took it to an independent repair shop, and got it fixed with a new, painted-to-match door for less than $1,000. The door fit and functioned perfectly, and there were no signs of an accident; my dad kept the vehicle for many years after that without any problem. The photo above shows how it looked when my dad sold it.

If The Car Is Cheap, It Doesn’t Take Much For It To Be ‘Totaled’

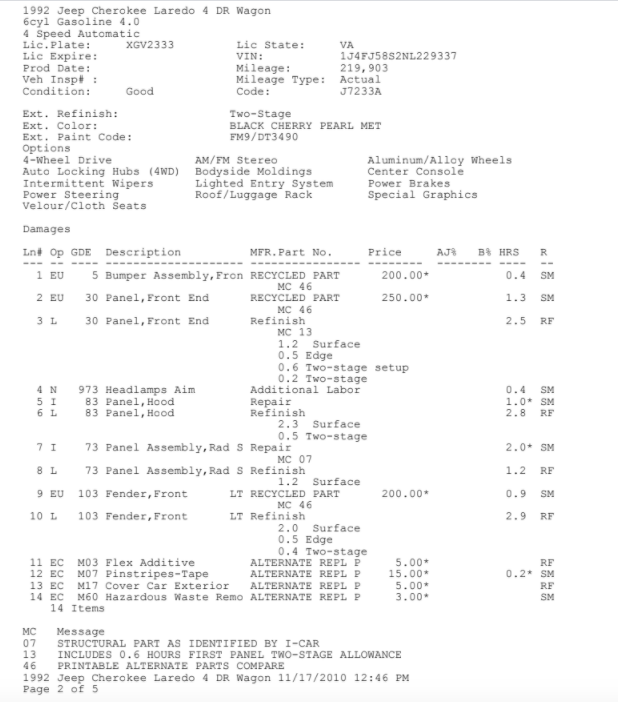

Sometimes this happens. A shop thinks damage is worse than it really is, it is just erring on the side of caution, or the vehicle really just isn't worth much, and they total a car out. Take my 1992 Jeep Cherokee (shown above); during my sophomore year in college, the vehicle took on front end damage thanks to a distracted Chevy Tahoe driver. Initially, I tried to work out a cash deal with the other party, so I got a few estimates from shops.

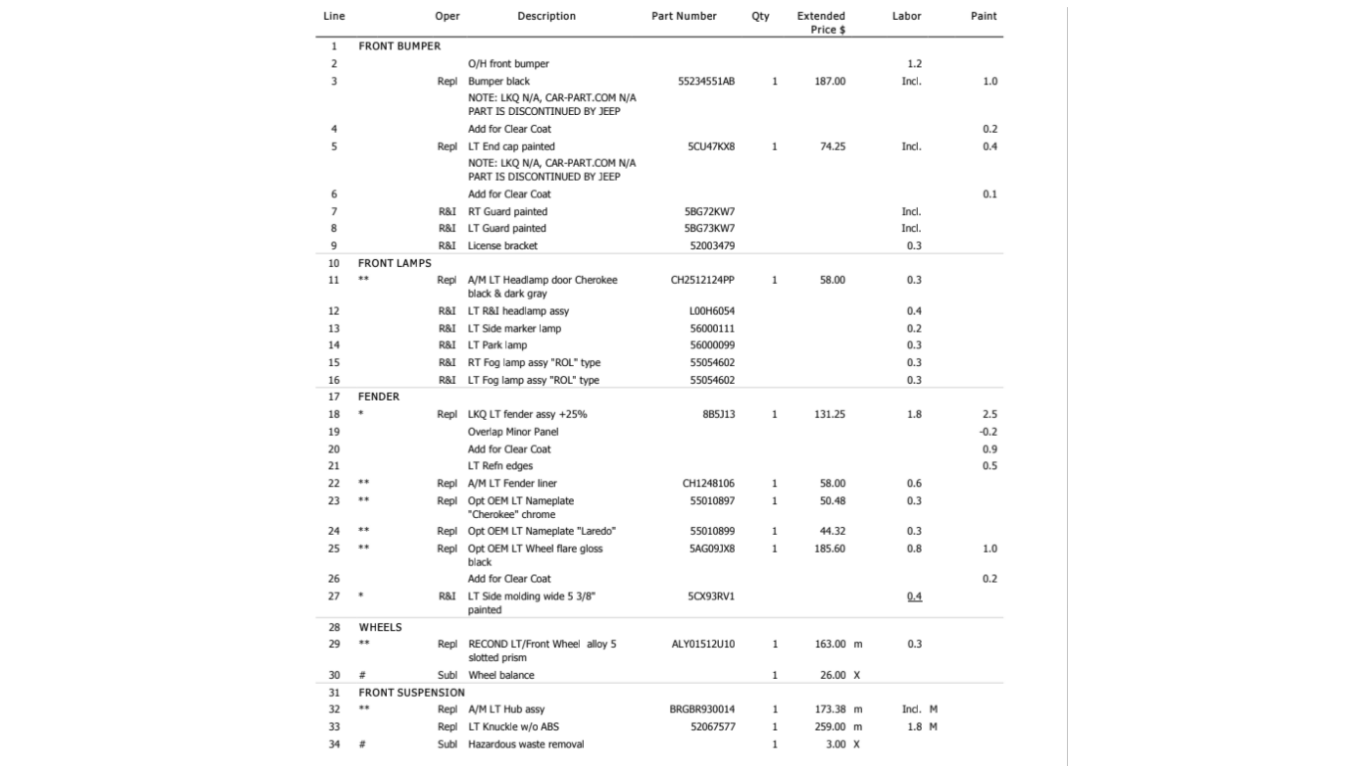

One outfit gave me an estimate of $2,800, and included 11 hours worth of labor for "unibody" pulls and radiator support repairs:

Another shop, which quoted me a whopping $3,451, also included unibody repair labor charges:

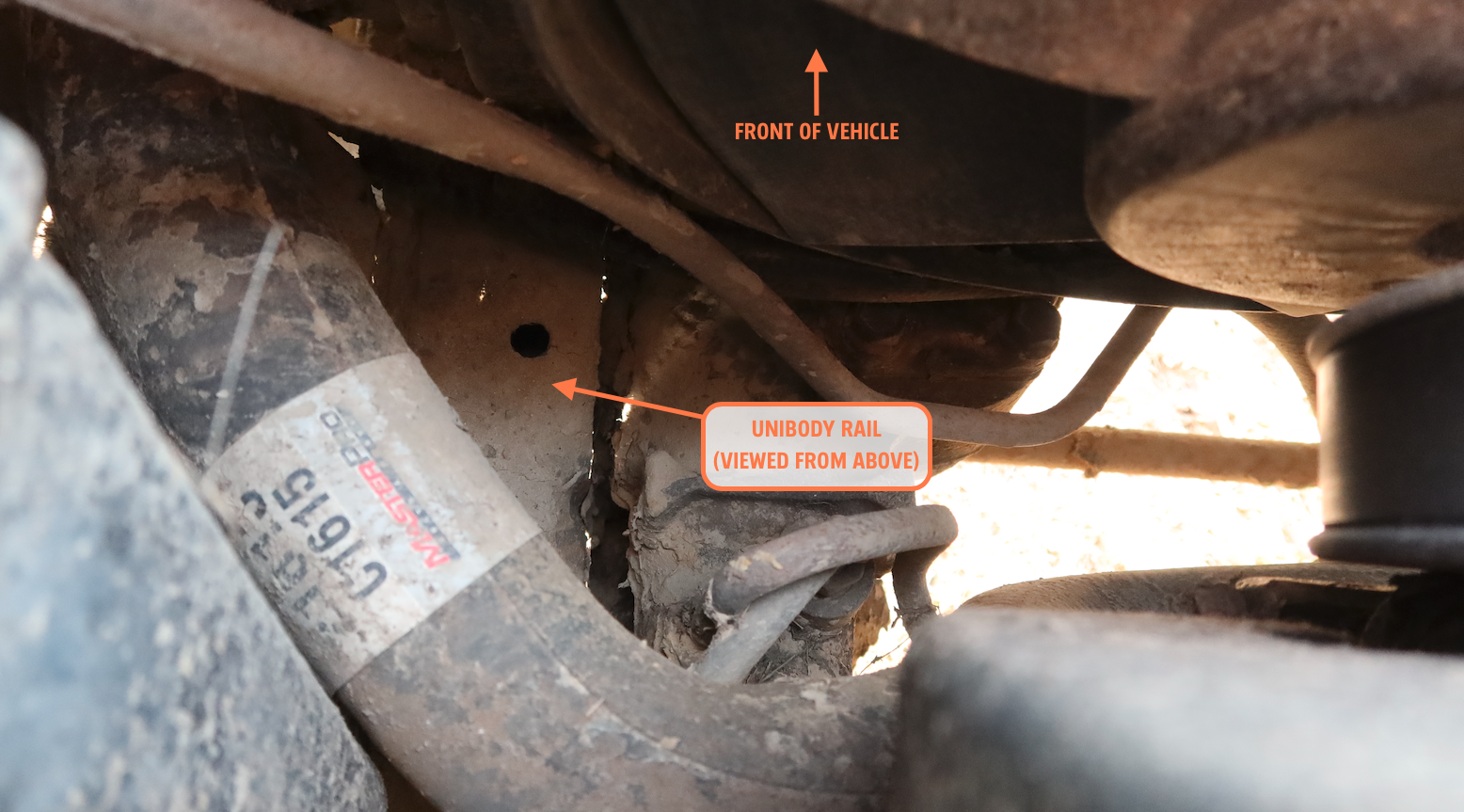

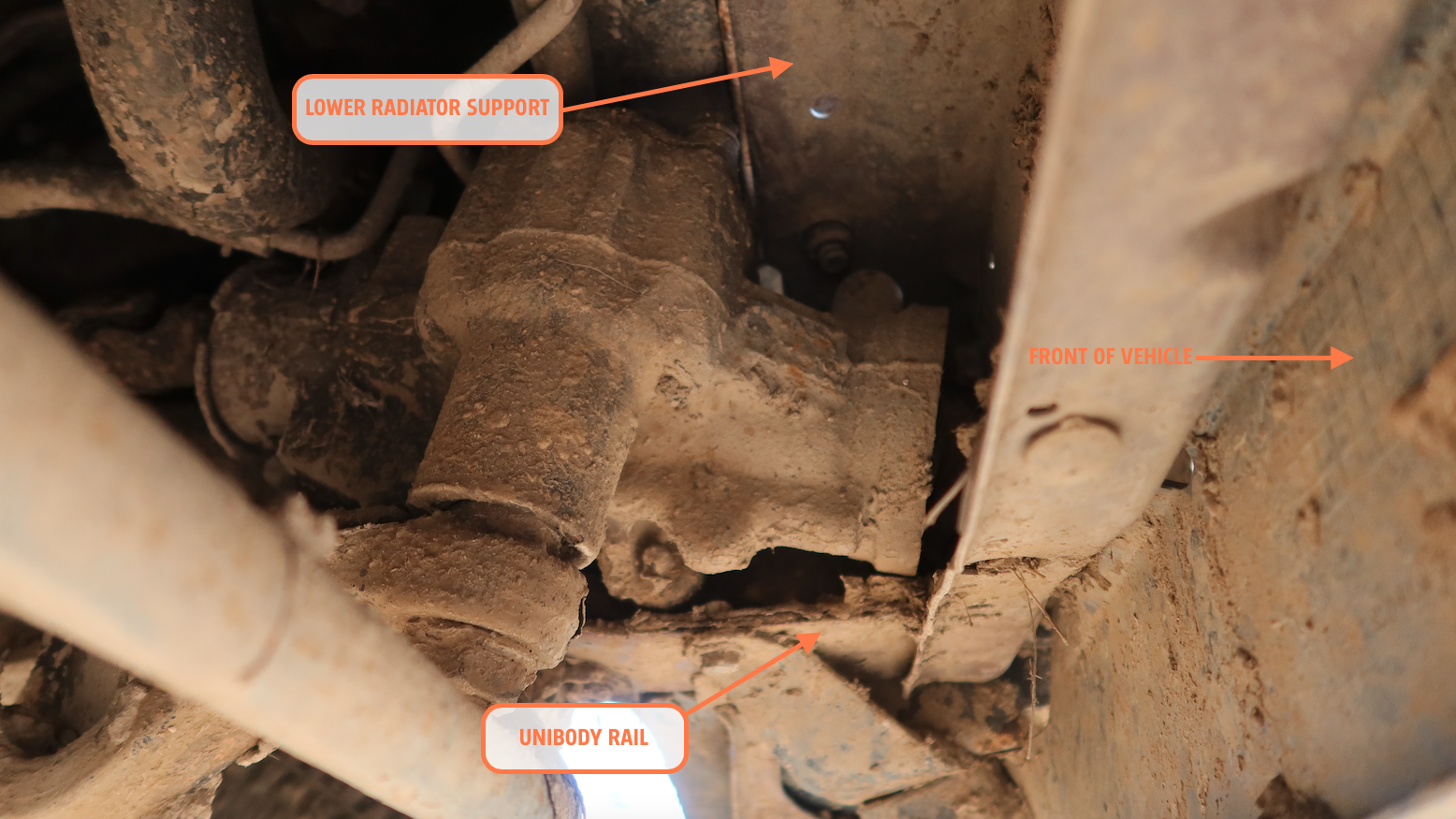

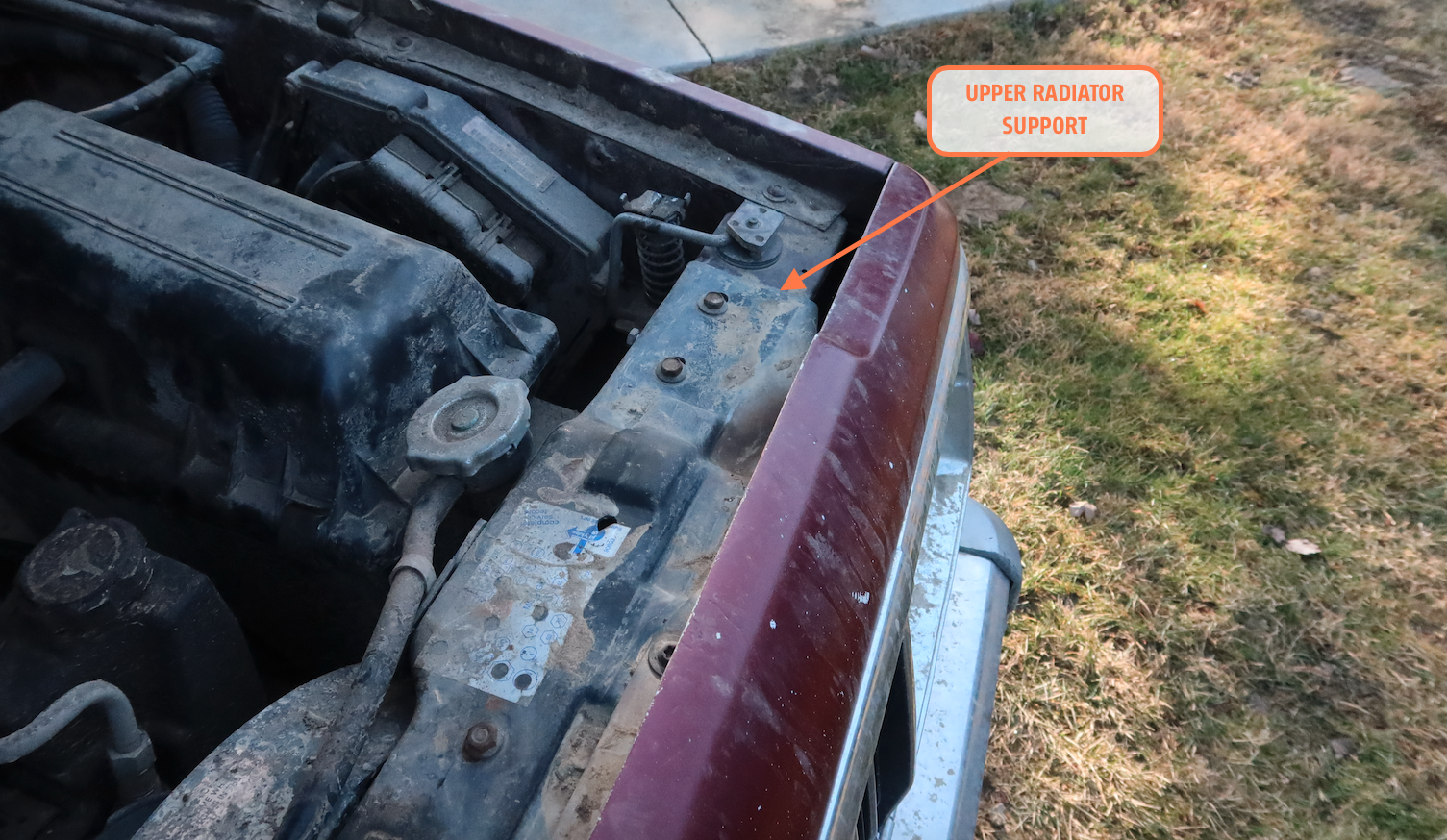

I've pulled that Jeep apart quite a few times since this crash back in 2010; I've even replaced the engine. So I can tell you with certainty that there is absolutely no unibody damage on this vehicle. These shops were quoting me for damage that didn't exist. Here, have a look at my unibody in these images, which admittedly, would be a lot more useful if they showed a vehicle that wasn't covered in mud from my off-road excursion six months ago:

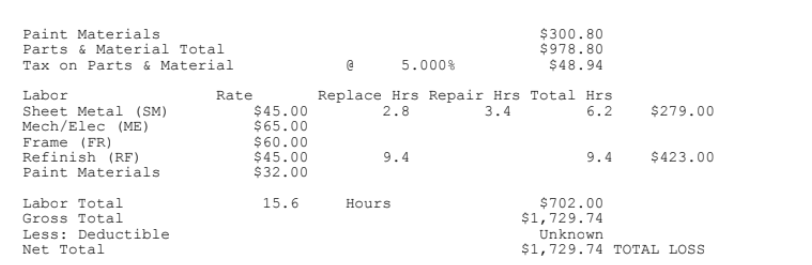

The good news is that, when my insurance company, USAA, had its official inspection done to see if the Jeep was worth fixing or if it was a total loss, the hired appraiser/insurance adjuster did not list any frame or unibody damage in the report:

Notice that the total cost of repairs was much cheaper than what was quoted by the independent shops I'd gone to:

Still, even though the insurance company's $1,730 repair estimate was less that what I'd heard from other shops, USAA ultimately deemed my beloved burgundy 1992 Jeep Cherokee a total loss. How did USAA come to this decision?

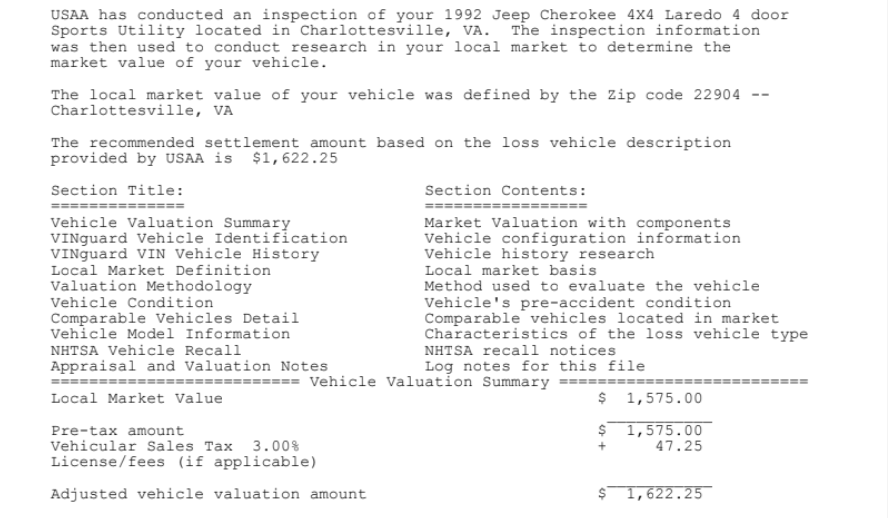

In addition to the repair estimate, USAA also provided me with a "Valuation Estimate," a document that basically showed how the company had looked into the local (Charlottesville, Virginia-area) market for similar 1992 Jeep Cherokees to determine how much a vehicle with my mileage, with my options, and in my pre-damaged condition was worth.

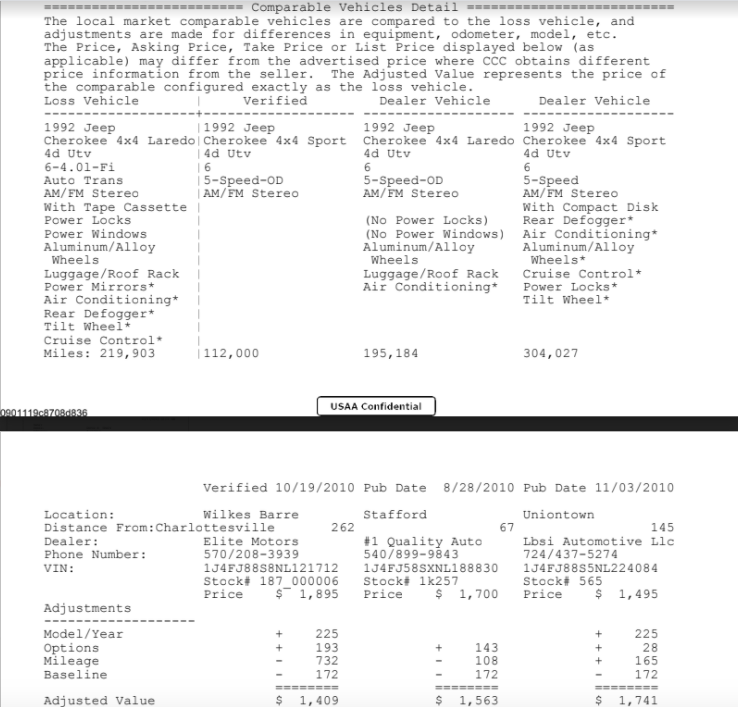

Here's a look at three vehicles for sale near Charlottesville, along with adjustments for mileage and options:

As you can see in the image above, Jeeps like mine were worth around $1,500, and as shown in the image before the one just above, USAA valued my vehicle at $1,622, which is less than the $1,730 damage estimate. Since fixing the car cost so much relative to the car's value, USAA deemed my Jeep a total loss. (More on what the exact relationship between the damage estimate and the vehicle value has to be to yield a "total loss" in a moment.)

I decided to hold onto the machine, since the damage looked manageable. I bought a bumper, fender and header panel, and fixed my Jeep for $300. The image above shows how the Jeep looked after my repair, and after some of my rattle-can job started flaking off the fender.

Clearly, repair costs to get a car back into original shape usually aren't cheap. The black, manual 1991 Jeep Cherokee that I bought a few years ago was no exception. It had a pretty nasty looking dent in the driver's side front fender, as you can see above, but otherwise, it looked mostly fine.

A look at the insurance estimate for the vehicle revealed why the car had been totaled: As was the case with my red Jeep, the black Jeep's damage meant repair costs were just too high for a car that had depreciated so low:

The costs are high for a number of reasons. First, all the replacement parts are brand new. It's worth mentioning that there are non-oem "alternative" parts offered, too, but those aren't exactly cheap, especially compared to what you yourself can find online or, especially, at a junkyard. Second, as is often the case, any part that has even a tiny scratch — like the front bumper, which looks totally fine sans a few little scrapes — is getting replaced. This sends the repair cost skyrocketing.

I reached out to USAA to learn more about how these estimates work, and how it leads to "totaling" a vehicle. "An insured is not permitted to remove or exclude loss related items to avoid a total loss – USAA is contractually obligated to put the vehicle back to a pre-loss condition," a representative told me. "An insured is allowed to withdraw the entire claim. Most states have laws and regulations that determine when a vehicle is a total loss – USAA is obligated to follow those laws and regulations."

"Insureds have the right to have their vehicle repaired at the shop of their choice if the vehicle is not deemed a total loss," the response continues.

So basically, you have three options: 1. Take the valuation amount as a check from the insurance company, and give the car to that company to sell at an insurance auction (possibly to a scrapyard). 2. Take the valuation amount minus what the insurance company could get at an insurance auction (the expected salvage value), and keep the vehicle and fix it — that's what I did with my burgundy Jeep. or 3. Withdraw the claim entirely and fix the car yourself.

In reference to USAA's statement about state regulations determining when something is a total loss, this generally comes down to the vehicle's Actual Cash Value (that's the valuation based on other vehicles on the local market) prior to the accident. In Michigan's case, a car is totaled if repairs exceed 75 percent of that value. From Michigan's Secretary of State website:

A salvage title is issued for a vehicle that has become a "distressed vehicle". A vehicle becomes "distressed" when one or more major component parts (such as bumpers, fenders, transmission, engine, hood, doors, frame, tailgate, body, etc.) have been wrecked, destroyed, damaged, stolen, or are missing to the extent that the total estimated damage is from 75% to less than 91% of its pre-damaged cash value. The vehicle owner's insurance company will determine the amount of damage to the vehicle. The regular title is replaced with a salvage title.

As demonstrated with my examples above, if a car isn't worth much, it's quite easy for it to become "totaled," even if it's totally fixable.

Titling And Insurance Of A Salvaged Vehicle

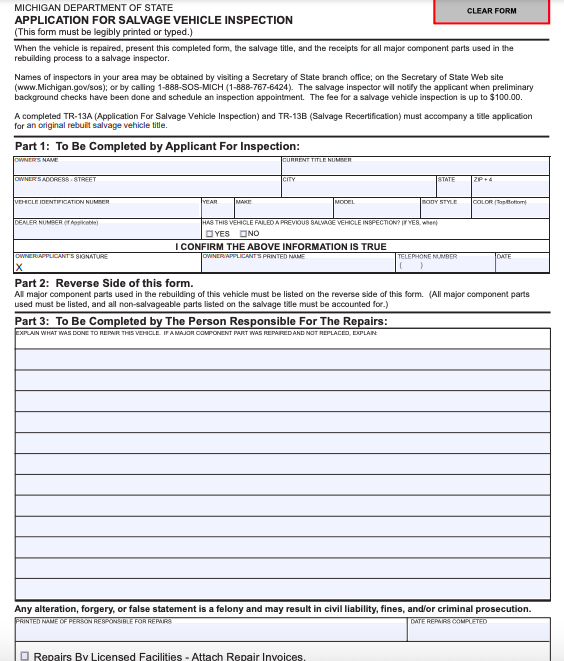

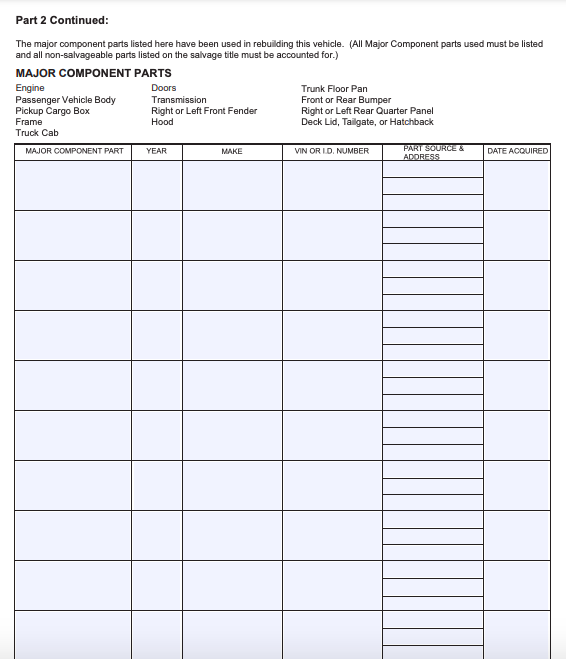

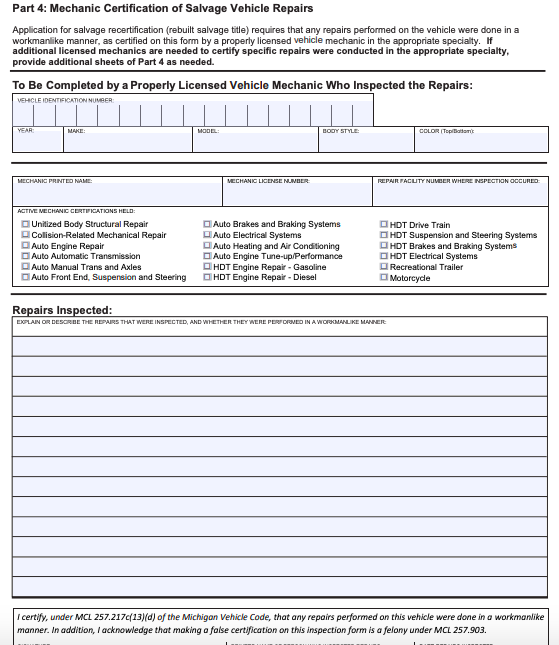

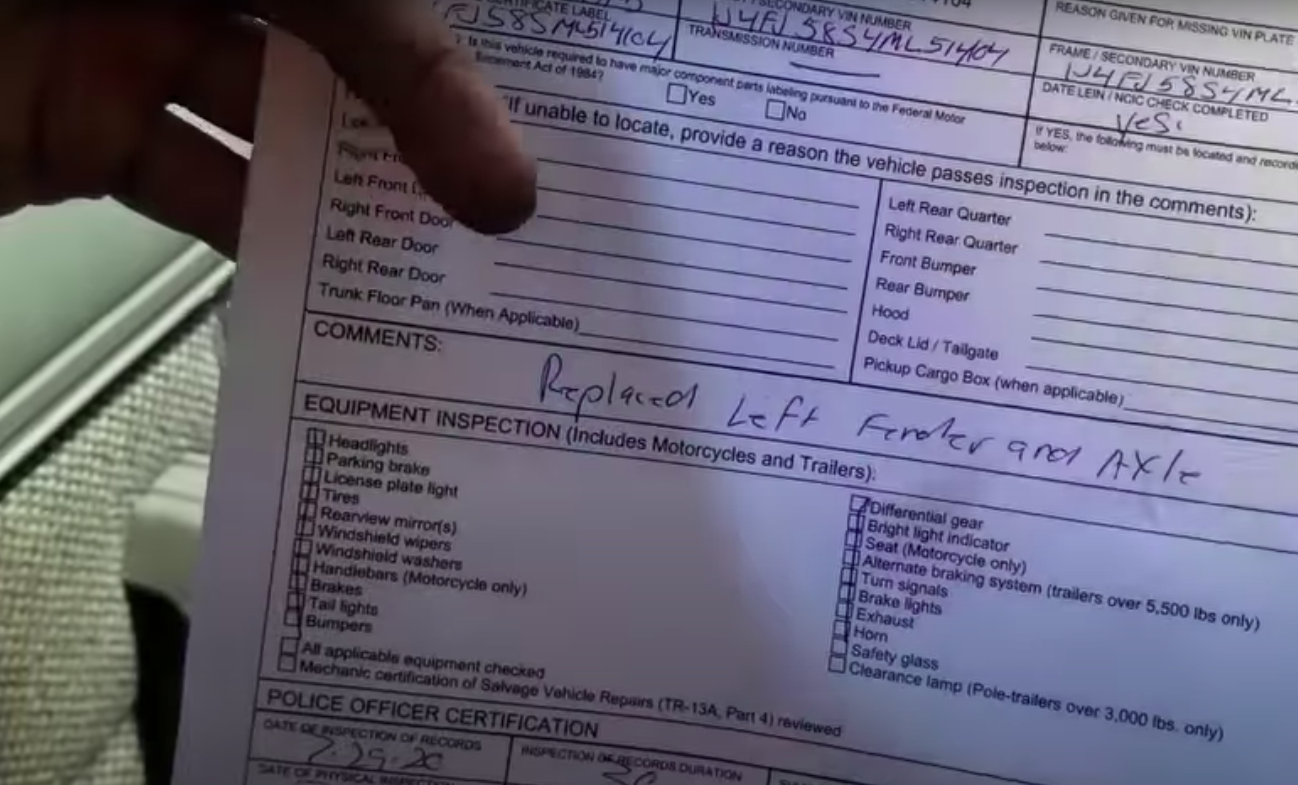

I was worried that titling my black 1991 Jeep Cherokee would be a difficult task, but it was quite simple. All I had to do is fill out the TR-13A form below — which required me to provide the source of every component I used to repair the vehicle — and take it to a certified mechanic, who made sure that the repairs had been done in a "workmanlike manner." Once that form was completed by both me and a mechanic, I took it to a salvage inspector.

Michigan's Secretary of State website has a database of local inspectors. I just called one inspector up, and met him at his house.

I hadn't fully repaired the Jeep, I'd just bolted on an aftermarket fender, figuring that would suffice in getting the vehicle looking complete.

I'd also swapped the front axle, because I was fairly certain it had bent at the outer "C" on the driver's side (the missing grease is, I think, where the C bent):

I let the inspector know about my repairs (he could also see them in the TR-13A form I gave him), he took a few looks at the Jeep parked on the side of the street in front of his house, and followed the following procedure:

1. Verify ownership of the repair parts used. The vehicle owner must present a properly assigned title or bills of sale for parts used in rebuilding the vehicle.

2. Inspect the vehicle to verify it complies with all Michigan Vehicle Code equipment and safety requirements.

3. Complete and issue a TR-13B form to the applicant.

The inspection was not thorough; the man did not spend lots of time (if any) under my vehicle. More than anything, this was just an inspection to make sure I hadn't used stolen parts to repair my machine.

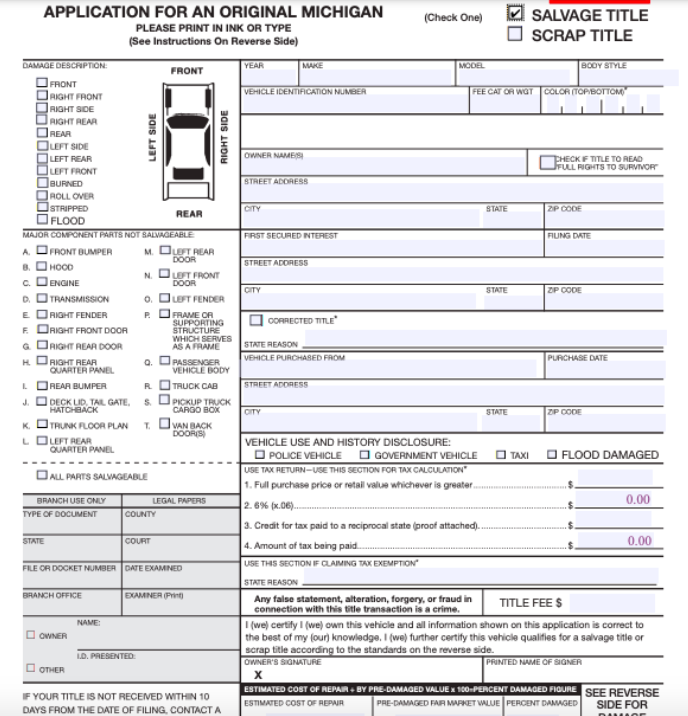

I then paid the inspector $100 for his services, before turning my Illinois salvage title (the one at the top of this section) into a rebuilt title. To do this, I took "TR-13B Salvage Vehicle Recertification form" that the inspector had given me, proof of insurance, the salvage title, and the Michigan title application form shown below to my Secretary of State office.

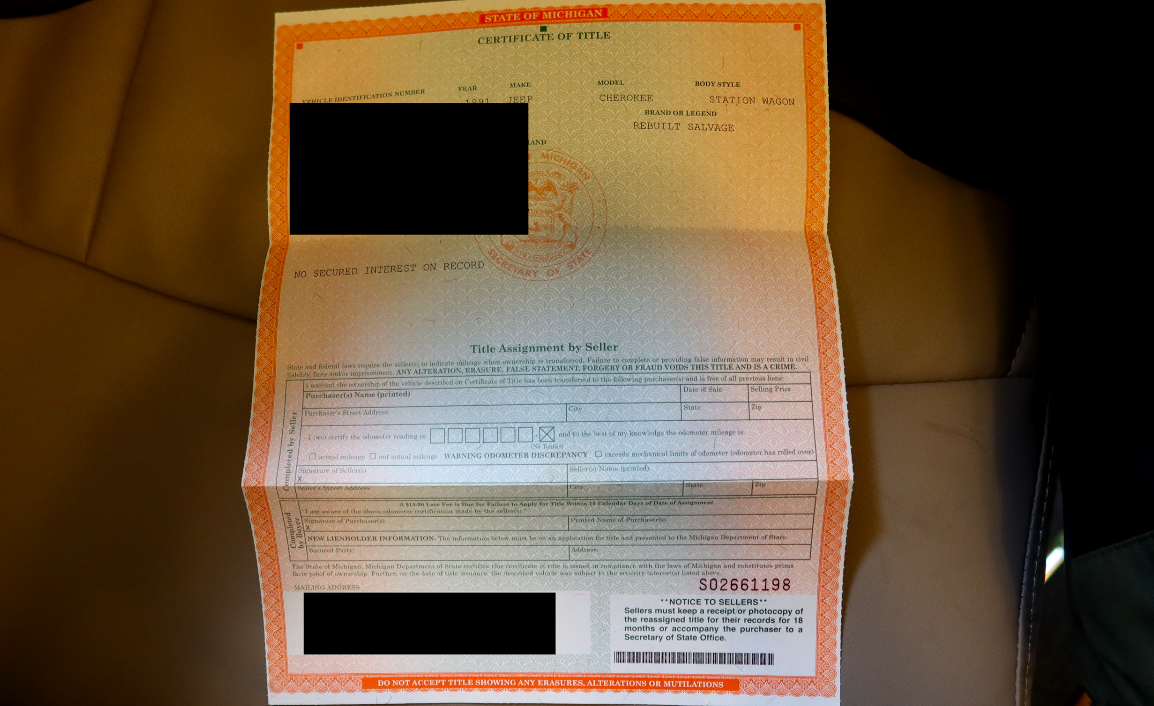

I received my registration and plates, so I could drive the Jeep legally on the roads. Within a few weeks, the rebuilt salvage title showed up in the mail:

Insuring a rebuilt car was no problem. I use USAA, and the rates were no different from a vehicle with a clean title as far as I could tell. Here's what State Farm told me about insuring a salvaged vehicle:

Underwriting is based on many factors. Simply having a salvaged vehicle or vehicle with damage, doesn't mean a driver can't get insurance from State Farm or that their policy will be canceled. Many vehicles that qualify as total losses can be restored by a qualified auto repairer.

If the car is worth more, and you want comprehensive coverage, that may be a bit trickier. But I'd be hesitant to buy a valuable car that's been deemed a total loss in the first place, because that could the damage is quite significant (or just that parts are egregiously expensive — it all depends).

Why This Jeep Was Such A Great Deal

A rust-free 1991 Jeep Cherokee with a manual transmission, in good overall condition, is worth over $10,000 to some people these days, and I only paid $2,000. On top of the vehicle cost, I dropped $250 to have the fender painted, plus $300 on the front axle, fender, fender flare, and bumper end cap. All in, I spent around $2,600 on what is now a nearly perfect Jeep Cherokee XJ.

The image above shows my Jeep Cherokee as it sits today. Here's how it looked before:

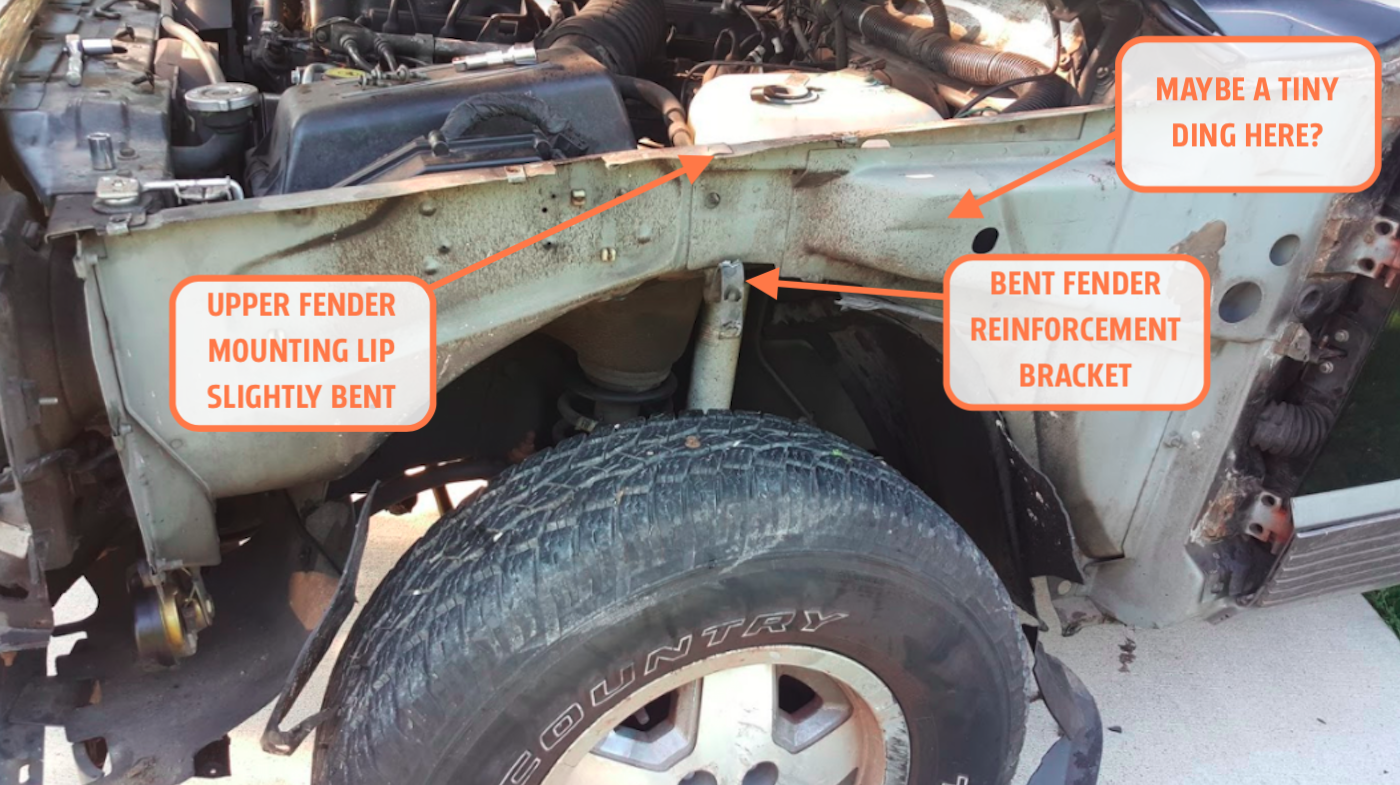

The vast majority of the damage was to the outer fender. When I removed it via 10 or 12 torx screws, it revealed an inner structure that was largely unscathed.

If you compare my Jeep's inner structure (above) with the inner structure of an un-crashed junkyard Jeep (see below) whose outer fender I snagged after deciding the aftermarket fender was no good, you'll notice that my Jeep made it out of that crash in fine shape. There may be a little ding on one part, and possibly some light bends in the sheetmetal where the outer fender bolts to the top of the inner fender (bends that I could easily get straight with pliers). Plus there was a bent fender reinforcement bracket that I replaced with one off the junkyard Jeep, but otherwise, my 1991 XJ looked great.

Here is a look at the fender I took off the junkyard Jeep shown above. I snagged a super-rare red spare tire carrier cover, which I can sell to offset the fender's $40 price tag. Partially hidden is a gold bumper end cap, which I needed, since my Jeep's silver one was missing.

Here I am prepping the junkyard fender for a paint job, which I farmed out to a local body shop (I just wiped the fender with alcohol to get grease off):

The body shop did a decent job, though for some reason, the technician didn't strip off the old pinstriping (I hadn't done it myself, because the shop told me not to worry about scuffing the fender for prep). So if you look at the car closely from certain angles, you can see the old striping, and the word "country."

I bolted that fender onto my Jeep, installed the silver flare, drilled out the bent reinforcement bracket and bolted the new one in, installed a new plastic wheel liner and carefully applied the red and white pinstripe stickers. There are some light dings, as the fender wasn't perfect to begin with, but I think overall, the Jeep looks great. The gold bumper end cap that I'd snagged at the yard and rattle-canned silver looks good, I think:

So in the end, I have a nearly mint Jeep Cherokee. Sure, the driver's side front wheel is scuffed, the rear bumper is pushed in a bit, and there is some bubbling on the bottom of the front fender. Plus, the hood is a little pushed in, yielding a bit of a gap between it and the fender:

But the interior is nearly mint, and the 4.0-liter straight six mated to the lovely five-speed AX-15 is in tip-top shape.

It's an incredible machine that, these days, I could not have scored for under $3,000 had it not been for the damaged fender.

A Vehicle With A Rebuilt Title Is Worth Less

Of course, this Cherokee is probably not going to sell for $15,000 on Bring a Trailer, not just because it's got a few imperfections here and there, but because the rebuilt salvage title itself lowers the vehicle's value, which makes the vehicle even more likely to be totaled out in the case of a minor accident.

Here's what USAA had to say about this topic:

If an insured retains a salvaged vehicle, they need to be aware of the following:A salvaged vehicle could be worth substantially less than a similar vehicle that has not been salvaged

Future claims will consider the salvage or other branded title and its impact on the actual cash value (ACV) of the vehicle Full premium will be charged for any coverages carried on a salvaged vehicle Reparability of a vehicle may change on any subsequent loss

Kelly Blue Book, an authority when it comes to vehicle valuation, says a rule-of-thumb on salvage titles is that value drops anywhere from 20 percent to 40 percent when compared to the same vehicle with a clean title. From KBB:

A salvaged, reconstructed or otherwise "clouded" title has a permanent negative effect on the value of a vehicle. The industry rule of thumb is to deduct 20% to 40% of the Blue Book® Value, but salvage title vehicles really should be privately appraised on a case-by-case basis in order to determine their market value.

So yeah, even though I scored a beautiful manual XJ for $2,600, it's not like I can flip it for five times that amount. Even though the vehicle is no different than a clean title Cherokee, the rebuilt salvage title reduces the machine's value, possibly because some folks are worried that the Jeep may have hidden structural damage.

What’s The Main Takeaway?

You should not be scared to buy a car just because it has been "totaled" and has a rebuilt or salvage title, but there are plenty of things you need to consider. First, get a hold of the insurance company's damage estimate. It should lay out all of the parts that need to be replaced, and can give you a good idea of how bad the damage is.

Based on my experience, an insurance adjuster doesn't really get in-depth with the inspection, so I'd take the vehicle to a reputable body shop to make sure there's nothing missing from the insurance company's report, and—critically—that the vehicle doesn't have permanent structural damage.

Also check your state laws on what the process is to register as "rebuilt" a vehicle that has had a salvage title. In my case, the process involved a simple $100 inspection. It may also be worthwhile to call your insurance company to see if it has any rules on insuring a vehicle with a rebuilt title.

In the end, knowledge about how insurance companies deem vehicles "total losses" should help quell your fears about inexpensive cars that have salvage titles. If a vehicle is appraised to have a value of only $2,000 or less, then you can understand that it's pretty easy for it to be deemed totaled, and it doesn't really mean the vehicle has damage that you should be concerned about. A wrinkled fender is all it took to total my black Jeep Cherokee, and $600 later, now the machine is back to 100 percent.