How Much Money Should I Put Down On A Car Loan?

As Jalopnik's resident car buying expert and professional car shopper, I get emails. Lots of emails. I've decided to pick a few questions and try to help out. This week we're discussing the ideal down payment for a loan, buying a car from a dealer who doesn't sell that brand, and which car to buy or keep when upgrading to something new.

First up, what is the ideal down payment for a car loan?

I've got a car buying question. What is the ideal amount for a down payment on a car? 100%, as much as possible, or is there a point of diminishing returns? I'm thinking of getting a new daily driver for $40-60k in the near future, new or CPO. I'm not a member of the "F-you money" class, but I could probably manage a down payment of up to $10k.

This is a question that comes up a lot, and it really comes down to a personal financial decision for the buyer. Unlike leasing, where you want to put as little down as possible, when you buy something there is often no such thing as "too much money down." For example, putting $10,000 in should mean you always have equity in the car, but not everybody can do that.

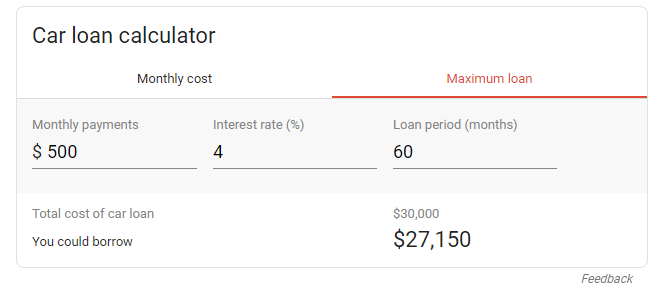

Most folks need to examine that down payment figure based on what their monthly payment target is. While you should never negotiate your car based on payment, you should be doing the math to see how much downpayment is necessary to fit that budget. Let's say, for example, you are buying a $40,000 car all inclusive of tax and fees and want to be at $500 per month with a 60-month loan and an estimated interest rate of 4 percent.

If we use our handy loan calculator and plug in the payment figures, term and interest, that means your loan balance can't exceed more than $27,150.

Which means you need to bring $12,850 to the table in order to get that $40,000 car within your comfortable monthly payment range. However, most folks don't have the cash to put 30 percent down on a car loan, which is why these backward calculators are crucial to establishing what you can afford before you start shopping.

Next, is a dealer more likely to cut a deal on a used car if they don't sell that brand?

"I had purchased a used 2016 BMW X5 about 6 months ago. There were particular features I was interested in, but the general prices I came across off Autotrader were about $35-45k for a mileage range of 30-50k. I ended up purchasing my vehicle from an Infiniti dealership, obviously through a trade-in by the previous owner. I jumped on the deal after some negotiation since it had all the features I was looking for. The KBB value for private party sale was about $38k. The dealer was selling it for $34k and was willing to give me the sale at $33k (taxes/titles/fees not included). At this time, for similarly spec'd vehicles, the average prices on Autotrader were still $3-4k higher than the Infiniti's dealership's original price. I purchased the vehicle after completing a pre-purchase inspection, did not trade in a vehicle, and did not finance through the dealership (had my own finance in place through a credit union).

Barring that all things are generally comparable and appropriate, was the Infiniti dealership willing to sell at a lower price in efforts to simply get a non-Infiniti brand car off their lot? If so, why is that? What advice are you able to share with readers towards considering purchasing a vehicle from a dealership of a different brand from the car itself?"

One of the common myths about used car buying that is still around is that a dealer that sells Brand A doesn't want to sell a car from Brand B. That is not really the case.

Dealers want to stock and sell desirable cars, regardless of the brand. The likely reason that this Infiniti dealer was able to offer a used BMW at a very competitive price is likely due to the market-based pricing for that particular car, and not really the fact that it was a BMW on an Infiniti lot.

As I've mentioned in several other posts, because online listings are competing against each other for leads, it is in the dealer's interest to come out of the gate with a sale price that is aggressive. Therefore they often don't have a lot of wiggle room, as you found out with that $1,000 reduction.

Chances are that the Infiniti store likes to move units quickly and prices them accordingly to make quick sales. While this might not mean a lot of profit per unit, it usually means more units sold within a shorter period of time.

There really is no unique strategy when buying a car from a dealer that doesn't sell that brand, and you did all the right things here. You looked at comparable cars, got the vehicle inspected, and came to the conclusion that the price you were offered was a good one.

Finally, when choosing between two cars to keep or trade, how do you decide?

"I'm in sort of a conundrum. I live in Orange County, CA and I commute to an office near LAX every day. I have either use my 2015 Subaru Forester XT or my wife's 2013 Lexus GS350. Both cars are paid off. I am thinking of selling one of the vehicles and getting a Model 3 to get HOV access and to destress using AutoPilot.

Any advice on which car to sell because we are looking to keep whichever for the long run plus a Tesla and is it better and more financially sound to just keep the two we have now?"

This is an interesting situation because we have two good cars, so determining which one to trade or keep is a challenge. On the one hand, you have a Lexus sedan and you plan on buying a Tesla sedan. Perhaps having a different style of vehicle like the Forester in the driveway would be ideal, especially if you have a need for a crossover with all-wheel-drive depending on the situation.

On the other hand, if you are looking at this from a financial perspective, the Forester is likely to command a higher trade/sale value relative to its original purchase price. The XT models are going for some serious money now that Subaru no longer offers a turbo Forester option.

Furthermore, a Lexus GS may be more likely to have lower running costs as that car ages due to its reputation for build quality. Remember, sometimes those turbo Subarus get pricey on the maintenance as they age.